The Debt Divide

How homeowners sink while some Rob Arkley companies use bankruptcy to weather the storm

By Ryan Burns [email protected] @RyanBurnsy

[

{

"name": "Top Stories Video Pair",

"insertPoint": "7",

"component": "17087298",

"parentWrapperClass": "fdn-ads-inline-content-block",

"requiredCountToDisplay": "1"

}

]

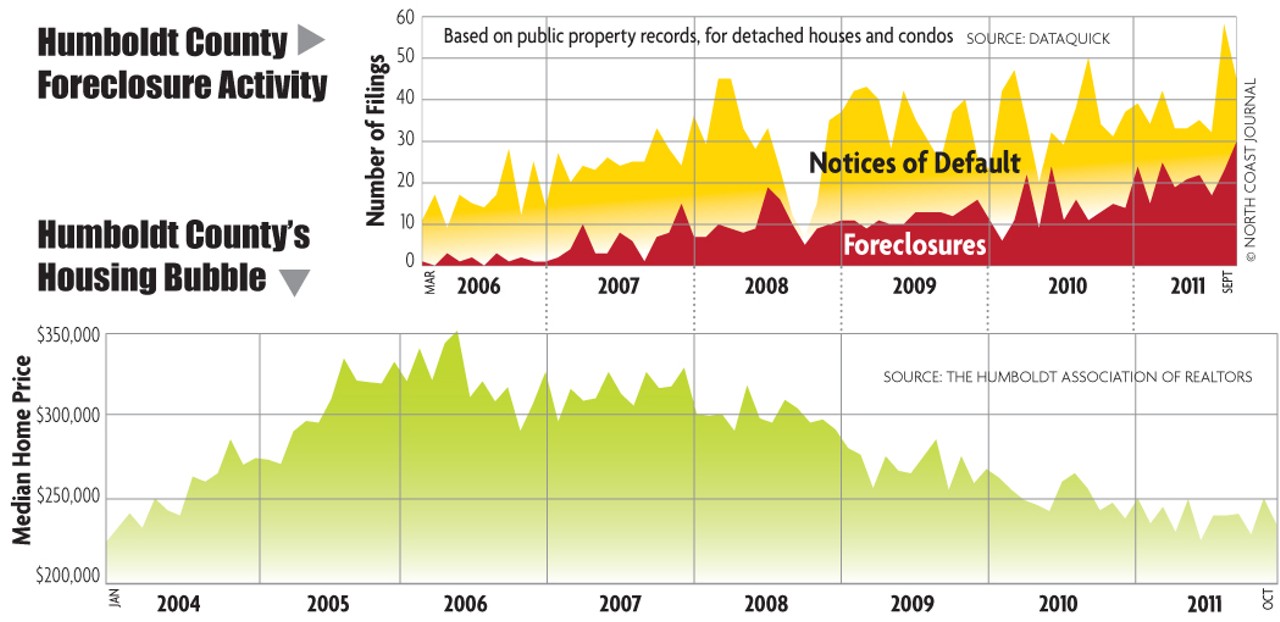

Since the local housing market peaked in March 2006, more than 700 homes have been foreclosed on in Humboldt County. That's about 25 foreclosures for every 1,000 single-family detached homes. Their owners almost invariably paid way too much, thanks to a real estate market that was speeding toward a cliff without seat-belts. Wall Street gimmicks like mortgage-backed securities and credit default swaps gave lenders a green light to issue blatantly irresponsible mortgages because the risk wasn't their problem. They immediately offloaded the hot-potato mortgages en masse to Wall Street investors. Home buyers, meanwhile, were assured by pundits and agents that housing prices almost never go down for long. They were encouraged -- even coerced -- into sub-prime mortgages by lenders so desperate for customers that many stopped asking for credit reports, or even checking for a pulse.

And when it all collapsed, everyone came out fine except the homeowners. Wall Street got its bailouts. Mortgage brokers got to keep the money they'd made. Ratings agencies and regulators who'd been asleep at the wheel got off with some mild public criticism. Lenders continued to demand every penny of the inflated home loans. But millions of homeowners lost their homes, and the foreclosure crisis is far from over.

Until about the middle of 2007, Humboldt County averaged just one or two foreclosures per month, according to information provided by DataQuick, a real estate information service. The foreclosure numbers have been climbing steadily ever since, reaching 10 per month in 2008, nearly 14 per month in 2010, and almost 22 per month during the first three quarters of 2011. Even today, the county's foreclosure rate isn't bad compared to the state average of 95 per 1,000 homes. On the other hand, Humboldt County wasn't exactly a hotbed of speculative investing; most of the foreclosed houses here had owners living in them.

And foreclosures only tell part of the story. Countless other homeowners owe more than their homes are worth, but continue paying their mortgage because they're afraid of the shame and guilt associated with foreclosure.

Eighty-one percent of homeowners believe it is immoral to "strategically" default on a mortgage, according to a 2009 survey by the National Bureau of Economic Research. It's an attitude they're encouraged to maintain. "The predominate message of political, social and economic institutions in the United States has functioned to cultivate fear, shame, and guilt in those who might contemplate foreclosure," Brent White, a law professor at University of Arizona, writes in his 2009 paper "Underwater and Not Walking Away: Shame, Fear and the Social Management of the Housing Crisis."

For businesses, the rules are different. Typically, their only goal is to maximize profit. If they can't pay their bills, they're not burdened by guilt. Nor do they face the same consequences as individuals. Last year, American Airlines filed for bankruptcy despite having $4 billion in the bank. It did so simply because its board decided it made good financial sense, and as James Surowiecki pointed out in The New Yorker, analysts agreed, calling it a "very smart" move.

Businesses can also structure themselves in ways that give them distinct advantages -- by incorporating in states with business-friendly laws, for example, or dividing their assets among their own sub-companies. That way, when creditors come calling, businesses have an array of protective mechanisms in place, and usually armies of lawyers to defend their wealth. Too often, in the American financial system, justice is afforded only to those who can afford it.

In Humboldt, this divide plays out on scales both intimate and grand, from one

Fortuna family to one of the biggest businesses in the county.

^^^^^^^^^^^^

In the summer of 2006, Fortuna natives Julie and Stephen Nally were ready for the last two basic ingredients of the American Dream -- homeownership and parenthood. The young couple had married two years earlier, and that August they found a cute little two-bedroom, one-bath house on Summer Street. It was barely 1,000 square feet, but it had a nice backyard and was in a good location, near the hospital, Safeway and Stephen's job.

"It was our picture-perfect little house," Stephen Nally recalled in a recent interview. The real estate market had been on an unprecedented four-year tear, but it had dipped in recent months and their agent suggested it was a good time to buy. Later -- too late -- they'd see that the dip was the start of a nosedive. They offered $235,500 -- more than $10,000 below the house's appraised value at the time -- and it was accepted.

With no money for a down payment, the Nallys needed two mortgages to finance the house. The first, for $188,400, was an adjustable-rate loan through Countrywide, starting with interest-only payments at just over 7 percent. The second, a $47,100 loan through a company called GreenPoint Mortgage Funding, had a fixed rate of 11.54 percent. Their monthly house payment came to about $1,500, which was doable. Stephen had a good job at Les Schwab Tire Center and Julie was a property manager at a local real estate office.

But less than a year after they moved in, tragedy struck. Julie had a miscarriage in her 24th week of pregnancy. Suddenly the house, which they'd been lovingly preparing for their new baby boy, was no longer a source of joy.

"We had, like, the crib in there. The room was painted. The baby clothes were ready. And then it wasn't there anymore," Stephen said. "We'd come home and ... we just didn't want to be there."

Julie agreed, so a month and a half later they moved in with Stephen's mom. Some friends agreed to rent the house for $1,200 a month, which meant that the Nallys were losing $300 each month. But they couldn't really ask for more money. Fair-market rent for a house that size was nowhere near their monthly mortgage payments. Even $1,200 was pushing it.

A few months later, Stephen got offered an assistant manager position at a new Les Schwab in Stockton. He remembers thinking, "Am I gonna stay around here and remember the stuff with our son, or am I gonna get the heck out of here and try to do something with our lives?" In February of 2008 they moved to a two-bedroom apartment in Elk Grove, where rent ran them another $1,100 a month. Still, they managed to make their house payments like clockwork -- until November. That's when their friends/tenants called to say they'd found a cheaper rental. They moved out with less than two weeks' notice.

The Nallys' apartment lease expired around the same time, and they moved to a house in Stockton, where rent was $1,500. Suddenly the Nallys had two $1,500 payments due every month, and no tenants to help pay the bills. They listed their house as an $1,100 rental, figuring that with that much coming in they could still make their house payments, barely. But no one in Fortuna was willing to pay that much. The Nallys were in trouble.

"We were living from paycheck to paycheck, trying to make it work, but it wasn't working," Julie said.

They stopped paying their mortgage and tried to negotiate with their lenders, which now included Bank of America (BofA acquired Countrywide in 2008). Stephen asked if they could lower the interest rates or maybe add payments onto the back end of the loan to allow time to find new renters.

"Bank of America wouldn't even give us the time of day," Julie said. Their other lender, GreenPoint, accused them of secretly renting out their house and pocketing the rent rather than making their loan payments, she said. "We're not backstabbing, dishonest people. We're trying to make a living. It was just crazy."

Over the next nine months they got three short-sale offers, meaning the amount offered was less than what the Nallys owed. All three were rejected by the lenders. When asked why, a spokesperson for Bank of America told the Journal that the offers were deemed too low. (The highest was $130,000.) GreenPoint couldn't be reached because it's no longer in business. (A lawsuit pending in Florida accuses the company of selling mortgage-backed securities that were supported by defective home loans.)

The lenders foreclosed on the Nallys' house in September 2009. Three months later it was sold at auction for $155,900. The Nallys have since moved back to Fortuna, where they pay $1,250 for a rental that they share with their three sons, aged 3, 2 and 10 months. Their finances, Stephen said, are "in the toilet."

The Nallys' story is not unusual. Rosie Wentworth, program development director at Consumer Credit Counseling Service of the North Coast, sees lots of people in similar situations. In 2009 her company started a foreclosure prevention counseling program, and Wenworth, the program's only counselor, sees as many as 10 to 15 new clients every month. "We could probably do more if we had more counselors," she said.

The Nallys' interactions with their lenders were pretty typical, Wentworth said. Loan modifications are notoriously difficult to get because, "Quite bluntly? The [lenders] make more on foreclosing on a house than they do on modifying the loan." And short sales are not only difficult to get approved, they also can leave the sellers liable for the remaining debt. "They're just not a good thing," Wentworth said.

California is one of 11 so-called "non-recourse" states, meaning banks can't hold borrowers liable for their mortgage debt if the house goes into foreclosure. But the foreclosure will stay on the Nallys' credit report for seven years. Wentworth said families that immediately start rebuilding their credit can potentially be approved for another home loan in two to three years. But the biggest impact she sees from foreclosures is not financial. "It's emotionally upsetting," she said. "It's traumatizing in many cases."

A few days before Christmas, Stephen and Julie Nally sat in their rented Fortuna living room while their boys crawled on the furniture and watched TV. Their fuzzy red stockings were tacked to the drywall beneath the breakfast bar, and an illuminated Christmas tree stood next to the gas fireplace. They said they'd like to buy a home again -- this very one, in fact -- but there's no way they could qualify for a loan. Now $20,000 in debt, they're seriously considering bankruptcy.

Sitting on his couch with two of his three sons, Stephen reminisced about being a homeowner. "It's like, 'This is it. This is life,' you know? What you see on TV all the time. It just didn't happen the way we wanted it to."

^^^^^^^^^^^^^

Security National's money troubles are far more complex, but then so is Security National. The privately held Security National Master Holding Co., headquartered on Fifth Street in Eureka, is parent to more than 130 distinct business entities, mostly "limited liability companies," or LLCs. Collectively these companies specialize in real estate management, loan acquisitions and loan servicing.

Why so many? Brian Mitchell, Security National's vice president of accounting and real estate, said it's common to set up a new LLC every time a new group of properties is acquired. This so-called "ring fencing" serves to wall off investments from one another. That way, if one LLC (or a group of them) falls behind on its debt payments, its creditors can't go after the assets of another LLC. In non-recourse states, home loans work in a similar fashion. If a homeowner defaults on her mortgage, the bank can take her house, but it can't go after her savings account or her car.

On Oct. 17, 2011, a group of 10 Security National LLCs filed Chapter 11 bankruptcy in Delaware. Together, these 10 companies own 33 commercial properties in 15 states -- mostly office buildings and shopping centers, plus two trailer parks, one in Wyoming, the other in Alaska.

These 10 LLCs make money by acquiring "underperforming commercial assets," then making them profitable through "aggressive leasing and cost-cutting measures," according to documents filed in bankruptcy court. This is Rob Arkley's specialty. The president and CEO of Security National started his company in 1987 when he bought a mortgage loan portfolio from a failed Alaska bank. The company then acquired "distressed assets" from government entities, according to Security National's website.

A "distressed" or "underperforming" asset is one that's not generating as much money as it's supposed to. In the case of mortgage loans that means the borrower isn't making his payments -- not on time, anyway. Most lenders view distressed assets as a hassle, but Arkley has made his fortune by seeking them out and making them pay.

In the chaotic aftermath of the economic crisis, however, the tables turned. Several Arkley companies under Security National Properties, a subsidiary started in 1996, found themselves saddled with debt and unable to make their loan payments on time. Before long, these companies had become underperforming debtors in somebody else's loan portfolio. And those lenders were threatening to foreclose.

Here are the facts as told by John Piland, Security National's chief financial officer, in a court declaration:

In October 2006 -- the same year the Nallys bought their house in Fortuna -- a number of Security National companies got a revolving line of credit for $200 million. There were multiple creditors, but Bank of America acted as the administrative agent.

Unlike the Nallys, Security National managed to get the terms of its loan modified on several occasions. The seventh amendment to the credit agreement, executed in April 2010, postponed the due date a full two years -- from January 2010 to January 2012. But there were conditions: Just like a home mortgage, payments had to come in on a set schedule: $8,050,000 by November 2010; another $12 million by February 2011; $10 million more by October 2011.

In order to make those payments, Security National needed to sell some of its commercial properties, and at the time of the seventh amendment it had a contract to sell the Northway Mall, a dated indoor shopping mall next to an airport in Anchorage, Alaska, for $34 million. But after the amendment was signed, Security National ran into the same problem faced by countless homeowners at the time: From a seller's perspective, the market sucked. Not only were values in the toilet but credit was tight.

The Northway Mall deal fell through. The buyer couldn't secure the closing funds. Security National had eight other properties listed for sale. Of those, it managed to sell two and make the first payment of $8,050,000 on time. But Security National officials weren't exactly happy with the state of the commercial real estate market. "Investors with cash were price gouging sellers that had no choice but to sell," Piland complained in his court declaration.

Bank of America suspected that Security National wouldn't make its second payment, and at a March 2011 meeting, bank officials told the company to sell every last piece of real property and pay the loan amount in full. This was the equivalent of foreclosing on a home loan. Security National officials argued that even if they did manage to sell all those properties, the price they'd get in the current market "could produce insufficient proceeds to repay the principle balance." In other words, they were underwater, just like the Nallys had been.

Bank of America won't comment, saying it wants to protect customer confidentiality. What's clear is that there's no love lost between BofA and Rob Arkley. In 2010 the bank sued Arkley and his wife personally for $50 million after Security National repeatedly defaulted on a group of so-called warehouse loans ("Arkley's Word," May 6, 2010). Without giving a reason, Bank of America dismissed that suit shortly after it was filed.

But now Arkley and his companies were in another standoff with BofA. Over the next several months, BofA and Security National worked to develop yet another loan restructuring agreement, but those negotiations came to an end on Oct. 7, 2011, when BofA informed Security National that it was gathering bids to sell its now underperforming loan "in the very short term." Six days later, the 10 Security National companies declared Chapter 11 bankruptcy, preventing Bank of America -- at least temporarily -- from selling the loan out from under them. Going into bankruptcy, Security National owed just under $160 million.

^^^^^^^^^^^^^^^^^^^

The 10 companies involved are merely business structures designed to protect assets. So these LLCs have no offices or employees of their own. (The parent company's properties division has 81 employees, 24 of whom are local.) Their headquarters are considered the Eureka offices of Security National, yet on paper, nine of the 10 companies are Alaska-based LLCs (though their mailing addresses are in Baton Rouge, La.). The one exception, confusingly, is Security National Properties-Alaska, LLC, which is based in Delaware.

This virtual map-hopping is deliberate. "Each individual state offers a different balance of tax, legal and accounting advantages, and we have professionals to advise us on where to incorporate," Security National VP of Accounting and Real Estate Brian Mitchell explained in a recent interview.

For any company looking to protect its assets (and name one that's not), Alaska is considered the best place to incorporate, according to Lee McCullough, a Utah-based asset-protection attorney. The laws there make it harder for creditors to foreclose on business assets, he said. Delaware, meanwhile, is widely considered the best place to file bankruptcy. Partly this is due to precedent: With a long history of bankruptcy filings, Delaware's bankruptcy laws are firmly established and therefore predictable. But bankruptcy courts there also have a reputation for being business-friendly. More than 60 percent of Fortune 500 companies are incorporated in Delaware. And since one of the 10 Security National LLCs is located there (on paper, anyway), the whole group can legally file bankruptcy in Delaware.

Again, these businesses make money through "aggressive leasing and cost-cutting measures." This rigorously thrifty approach has affected the residents of Aspen Park, a bleak trailer court on the dusty plains outside Casper, Wyo. Nearly 200 corrugated metal trailers are arranged like piano keys around the elbows and cul-de-sacs of the park, which sits on a triangle of land between two freeways and a reservoir.

Though the residents themselves were unaware of it, many of them are listed among the creditors in Security National's bankruptcy case. Tenants must pay a $550 security deposit when they move in, and since companies must list every single creditor in bankruptcy filings, the names of Aspen Park residents ended up on court documents next to retailers, insurance agencies, construction companies and various state and municipal tax collectors.

Ralph Caughie and his wife Jackie pay $550 a month to live in "The Aspens," as locals call the park. In a phone interview last month, Caughie called the place a "rip-off" and a "slum court."

"My wife was sitting on the toilet when it fell through the floor," he said. Management eventually rebuilt the rotted floor, he said, but "I had to get on 'em three or four times before they got the right toilet." Before being contacted by the Journal, Caughie and other residents had never heard of Security National. They said they walk their rent money down to the manager's trailer once a month, and they were surprised to learn that their names were on court papers in a Delaware bankruptcy court.

Asked about the trailer park, Mitchell said employment is booming in and around Casper thanks to a natural gas boom (a boom fueled by hydraulic fracturing, or "fracking," which has caused groundwater contamination in the area, according to a December report from the Environmental Protection Agency). Mitchell said he hadn't heard about Caughie's wife falling through the floor while on the toilet, and he didn't agree with the characterization of the park as a slum court. "Is it the nicest place in town? Absolutely not. But I've been there. We provide the most affordable housing in the greater Casper area." It is, he said, housing for the "working class."

Mitchell said he anticipates that the company's creditors, including the tenants of Aspen Park, "will be paid 100 percent of what they're owed after this is resolved."

That's a tough thing to guarantee, according to Stanford Law Professor G. Marcus Cole. The goal in a Chapter 11 bankruptcy case is to give the debtor a fresh start, after submitting to a plan of reorganization. Security National would like that reorganization to be simply another extension on its loan agreement, but that is up to the judge. Fewer than 10 percent of Chapter 11 filings result in a confirmed plan of reorganization, Cole said.

Among the many requirements for such a confirmed plan, the judge has to believe that the business is viable -- that it will eventually turn a profit and repay its debts. The largest unsecured creditor in this case is an Omaha contracting/architectural products company called AOI Corp., which is owed more than a million dollars. Could they and the roughly 1,400 other creditors to these 10 Security National companies wind up shortchanged, or even empty-handed? Could the working-class people in Aspen Park lose their security deposits?

Cole hasn't reviewed the specifics of the Security National case. But in general, he said, who gets how much after a bankruptcy "really depends on the asset pool." Secured creditors -- those whose investments are tied to real property -- get priority. Real estate security deposits are included in that category. So is the line of credit that BofA wanted to sell. But other debts must be paid even earlier, including the administrative fees for the bankruptcy case, unsecured taxes and employee wages. For the people in Aspen Park, Cole said, "There's always the possibility that they won't get anything."

^^^^^^^^^^^^^^^^

As punishment for getting into debt they did not repay, the Nallys have been cast into a sort of financial purgatory. The blow to their credit will affect their ability to get new loans at reasonable rates; the issuers of their credit cards can jack up interest rates because they're now considered a greater risk; and they may encounter the social stigma attributed to people who walk away from their home loans. It will take them years to recover.

Security National doesn't have those problems. If bankruptcy proceeds the way company officials insist that it will, the companies involved will emerge not with a blow to their financial position but with another loan extension, and all of their assets intact. In the meantime, as the parent company confidently declared in the press release about the bankruptcy filing, "All day-to-day operations and business of all the Company's properties will continue as usual."

Comments (41)

Showing 1-25 of 41

About The Author

Ryan Burns

Ryan Burns worked for the Journal from 2008 to 2013, covering a diverse mix of North Coast subjects, from education, politics and marijuana to human suspension, sex parties and amateur fight contests. He won awards for investigative reporting, feature stories and news coverage.

more from the author

-

Last Days of the Surfing DA

Heading into his final year in office, Paul Gallegos talks politics, family and The Smiths

- Jan 2, 2014

-

Unequal Opportunities

Behind the ACLU's allegations of racial, sexual and disability discrimination in local schools

- Jan 2, 2014

-

Systematically Misled

- Dec 26, 2013

- More »

Latest in News

Readers also liked…

-

Through Mark Larson's Lens

A local photographer's favorite images of 2022 in Humboldt

- Jan 5, 2023

-

'To Celebrate Our Sovereignty'

Yurok Tribe to host gathering honoring 'ultimate river warrior' on the anniversary of the U.S. Supreme Court ruling that changed everything

- Jun 8, 2023

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}